The past years have emerged as a significant time for artificial intelligence (AI) and its democratization, shifting from enterprise use to the introduction of generative AI and its most known application – ChatGPT to the general public. The unveiling of ChatGPT and its perceived leap in capabilities pushed the whole AI sector forward creating a global “hype” that is still growing.

When talking about AI, there are a few terms that can cause confusion. AI usually refers to a tool that can analyze data, while generative AI can use the same analysis to create new and personalized content, products, features, and many more new and exciting things.

After the pandemic tech boom of 2021, the bubble burst and the pandemic hit Big Tech. Big Tech’s life raft, the launch of ChatGPT, created an influx of funds, above $40 billion, into AI start-ups while other Big Tech sectors continue to witness dry spells of this post pandemic slum.

Among this AI influx, one domain stands out – finance and insurance. With financial institutions expected to spend nearly $100 billion by 2027 (up from an approximately $17 billion during 2022) in AI technologies. While this is good news for the domain, or customers begging for innovation and advancements in a relatively conservative one, it’s not easy teaching an old dog new tricks.

Three main hurdles emerge: accuracy, accessibility, and execution.

First, financial companies are required to provide precise and accurate services to their clients, based on factual information and trustworthy decision making. The tolerability for errors from clients is non-existent, and current AI tools have not been proven to be completely errorless, with examples of hallucinated results abundant.

Second, AI’s life source, data, and more specifically financial data, is confidential and inaccessible, mostly entangled in regulation and security protocols. With AI tools requiring vast amounts of data, such privacy restrictions inhibit the ability to freely share and accumulate data between institutions, meaning, innovation in the sector is contingent on the willingness of large legacy incumbents to participate. Using such information and combining it into a program which is widely accessible and often exposed to open-source software is perceived as risky, and not aligned with the domain’s conservative approach.

Finally, financial institutions have struggled in the past to execute effective digital transformation processes as well as integrate new solutions into their current legacy IT systems. One notable example is the domain’s lag in implementing cloud services and infrastructure, which could have been an enabler for AI implementations as well. The financial domain appears to exhibit a certain hesitancy in embracing novel technological tools, especially when they entail major changes like AI applications.

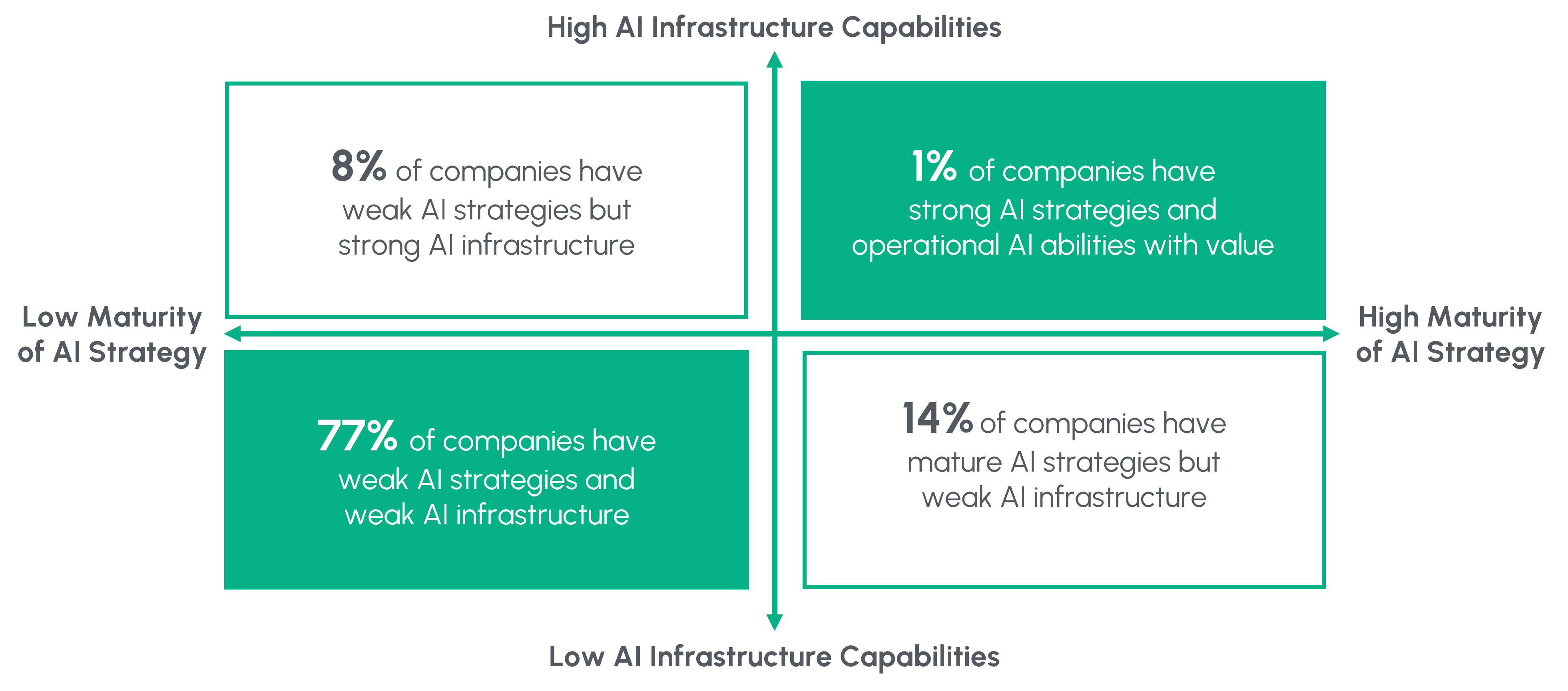

As seen below, recent surveys show that many companies remain inadequately prepared to implement AI solutions, with the domain lagging behind not only in essential infrastructure to seamlessly integrate AI tools, but also in terms of formulating strategic plans for their successful execution.

However, teaching an old dog new tricks is always made easier with some reward.

The opportunities for financial entities that incorporate AI solutions are too significant to overlook. Early birds are set to catch their worm through increased revenues, driven by operational efficiencies, enhanced marketing and sales strategies, and the personalization of financial offerings to clients.

Even legacy institutions, both Morgan Stanley and Goldman Sachs have acknowledged the importance of integrating AI processes and have made substantial investments in new generative AI tools to improve their offerings and their operations. To manage the current risk entangled within generative AI, these companies focused on employee-facing solutions which eliminate the fear of uncontrolled machine decision making, such as enhancing the analysis capabilities of financial experts within the bank. They also focus on chat interfaces for communication and advisement to clients on common enquiries that do not require decision making processes.

These focus areas will change over time through trial and error and as new developments are introduction, and time will tell what else the future holds as cautious players begin to dip their toes into AI. The path ahead may be challenging, but for those who navigate it well, the rewards could be immense. After all, it’s never too late to teach an old dog new tricks.

Proof can be found in Israel – just in the past few years, two new digital banks have been established, signaling even more innovation and progress ahead. HS predicts that the local market will continue to make use of both its AI startup ecosystem, while small is repeatedly ranked as a hub for development and use cases, and its word-leading fintech community which encompasses some of the largest and most prominent companies to create unique solutions.

This natural collaboration between local AI experts and the fintech community, is sure to create endless possibilities for the finance domain.